Why Digital Assets Require New Risk Models in Finance

Traditional risk frameworks were designed for assets that settle in days, leave paper trails, and fail slowly. Digital assets do none of those things. Understanding why digital assets require new risk models is not about discarding decades of sound risk management theory. It’s about recognizing that the data inputs, evidence patterns, and operational failure modes are genuinely different. This guide explains where existing models fall short, what needs to be added, and how finance and risk professionals can adapt without starting from scratch.

Table of Contents

- Key takeaways

- Why digital assets require new risk models: the data transparency factor

- Operational and technological risks with no traditional equivalent

- Automation and machine-speed decision-making

- Regulatory capital requirements and model defensibility

- Practical steps for adapting risk models

- My take on building risk models that actually hold up

- Sharpen your digital asset risk readiness with DARE

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Different data, not different theory | Blockchain’s transparent ledgers change risk inputs, not the foundational principles of risk management. |

| Operational risk is programmatic | Smart contract bugs and oracle failures can trigger irreversible losses in seconds, requiring real-time controls. |

| Automation is now a compliance requirement | The volume of on-chain transactions exceeds human review capacity; automated decisions must be explainable and auditable. |

| Regulatory capital costs are already here | Basel III assigns a 1250% risk weight to crypto assets, making model defensibility a capital efficiency issue. |

| Unit of analysis must shift | Scoring at the wallet and flow-graph level, not just counterparty level, is required to detect modern obfuscation methods. |

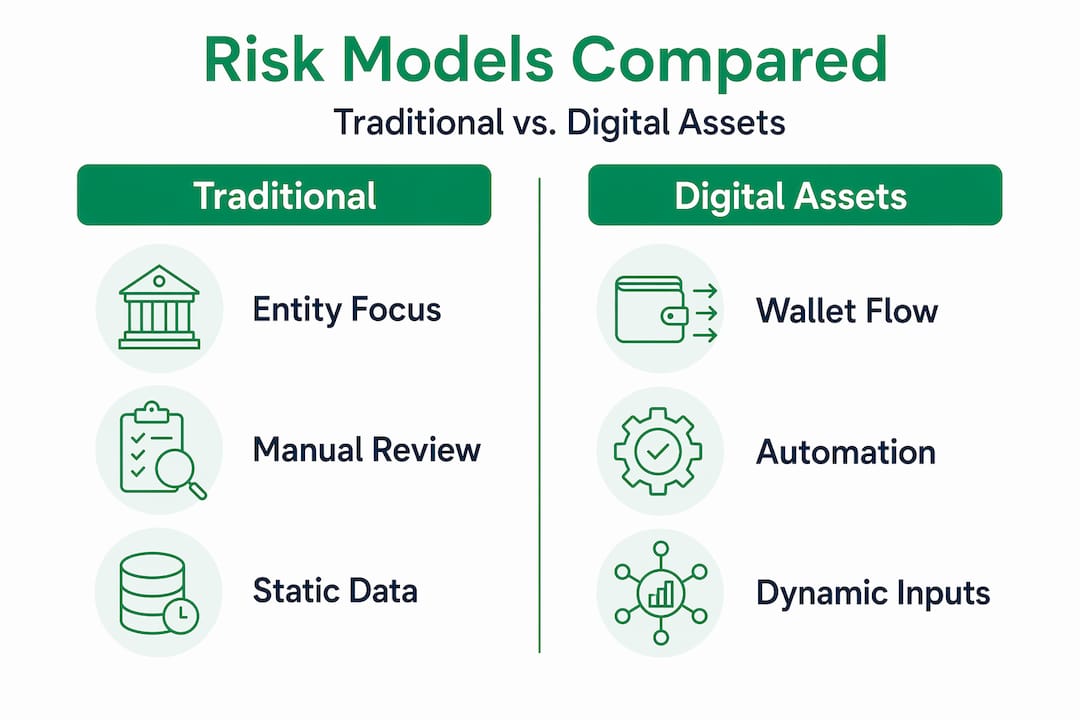

Why digital assets require new risk models: the data transparency factor

The most underappreciated difference between digital assets and traditional finance is not volatility. It’s the nature of the underlying data. Blockchain analytics allow tracing across dozens of hops, exposing fund movement patterns that are completely invisible in fiat transaction systems. That’s not just a compliance advantage. It fundamentally changes what risk measurement inputs are available and what models need to process.

In traditional finance, you see the counterparty and the amount. In blockchain environments, you can see the entire prior history of a wallet, every intermediate address it touched, and the originating exposure from transactions that happened months earlier. That level of data depth demands a model architecture designed to consume and interpret it.

The obfuscation tactics have evolved to match. Cross-chain laundering and chain peeling break transaction trails across wallets and chains in ways that closely resemble smurfing in traditional finance, but at machine speed and across multiple blockchains simultaneously. A model that only looks at direct counterparties will miss the origin exposure entirely.

Some specific evidence patterns your risk model must account for in blockchain environments:

- Multi-hop fund flows where illicit exposure travels through five or more intermediate wallets before reaching your institution

- Cross-chain bridges used to obscure origin by converting assets between incompatible ledgers

- Chain peeling where large amounts are broken into smaller, sequential transactions to reduce visibility

- Mixer and privacy coin exposure detectable only through probabilistic flow analysis, not direct address matching

Pro Tip: When evaluating blockchain analytics solutions, require the vendor to demonstrate multi-hop tracing across at least five wallet hops and cross-chain detection before signing. Single-hop scoring tools will produce systematically blind risk assessments.

Operational and technological risks with no traditional equivalent

Standard operational risk models capture human error, process failure, and fraud. They were not built to handle code that executes autonomously at the speed of a block confirmation. Smart contract bugs and manipulated data feeds can produce losses in seconds, with no opportunity for post-facto intervention. The irreversibility of blockchain settlement makes this categorically different from a failed SWIFT payment.

Consider the oracle manipulation problem. A price oracle feeding a lending protocol can be exploited to inflate collateral values. The attack, the liquidation, and the asset drain can all occur within a single block. No traditional operational risk control catches that. No manual review process operates at that speed.

Effective digital asset risk management requires securing protocols with deterministic, on-chain guarantees rather than relying on legal contracts or post-event remediation. That’s a structural shift in how operational risk is conceived, not just a new line item on an existing model.

Risk model components that traditional frameworks are missing in this context:

- Code audit status tracking as a living input, not a one-time diligence check

- Oracle source diversification scores to measure data feed concentration risk

- Bridge protocol exposure limits reflecting the outsized hack frequency on cross-chain infrastructure

- Real-time transaction monitoring that flags anomalous on-chain activity before settlement finalizes

Pro Tip: Circuit breakers that pause protocol interaction when anomalous transaction volumes or price deviations exceed thresholds are among the most practical active controls available. Monitoring the mempool for pending large transactions can give your team seconds of lead time before an adversarial transaction confirms.

Automation and machine-speed decision-making

The volume problem is not theoretical. On-chain risk decisions now exceed what manual analyst teams can process, and that gap is widening as institutional adoption grows. This forces a shift from risk scoring as an analyst tool to risk scoring as an automated, operationalized control layer.

But automation in this context carries a specific regulatory expectation. It’s not enough to produce a score. Regulators expect traceable reasoning and data lineage behind every automated decision, meaning your model outputs must be explainable, reproducible, and tied to specific evidence. This is what separates defensible risk automation from a black box that creates more regulatory exposure than it solves.

The progression toward agentic models in digital asset risk follows a clear sequence:

- Automated screening at transaction ingestion, applying policy rules and risk scores without human intervention

- Anomaly escalation where AI-flagged cases route to human analysts with evidence pre-assembled for review

- Documented decision trails where every automated outcome includes the specific on-chain evidence, policy reference, and scoring logic used

- Model validation cycles that test decision quality against regulatory examination scenarios, not just historical accuracy

The goal is not to remove human judgment. It’s to apply human judgment where it adds value and automate where volume makes manual review impossible. For professionals responsible for enterprise crypto risk oversight, building that governance layer around automated systems is now a core competency.

Regulatory capital requirements and model defensibility

The regulatory pressure is not coming. It’s already here. Basel III finalizes a 1250% risk weight for BTC and comparable crypto assets, which means an institution holding $10 million in Bitcoin must hold $1.25 billion in risk-weighted assets against it under the standard approach. That is punitive by design, and it creates an immediate incentive to build the kind of granular, documented risk models that could support a more favorable treatment over time.

The comparison between traditional and digital asset risk modeling under current regulatory expectations makes the gap concrete:

| Dimension | Traditional asset models | Digital asset models required |

|---|---|---|

| Data inputs | Balance sheet, credit ratings, historical pricing | On-chain flow data, audit trails, smart contract status |

| Risk weight basis | Asset class and issuer credit quality | Regulatory prescribed weights (up to 1250%) |

| Evidence standard | Documented methodology | Traceable, reproducible, evidence-backed decision logs |

| Operational risk scope | Human error, fraud, process failure | Code failure, oracle manipulation, bridge exploits |

| Model update frequency | Annual or event-driven | Continuous, given protocol and market evolution |

The regulatory direction is toward more scrutiny, not less. Professionals responsible for monitoring digital asset market risk need models that can withstand examination, not just produce internally useful scores.

Practical steps for adapting risk models

The adaptation of risk models for digital assets does not mean building a parallel framework. It means systematically updating the components that the existing model assumes away. The following areas require deliberate action:

Shift the unit of analysis. Traditional models score at the legal entity or account level. Models focusing only on counterparties miss laundering origins entirely. Wallet-level and flow-graph-level scoring is the minimum required to detect modern obfuscation techniques. This applies directly to your digital asset liquidity risk assessment processes as well.

Incorporate forward-looking cyber threats. Quantum vulnerabilities could amplify incident severity due to blockchain’s immutability. A post-quantum attack on a private key is not recoverable the way a compromised bank credential is. Model your cyber risk scenarios accordingly.

Replace static models with dynamic frameworks. Scenario analysis and standardized data reporting are improving across the industry precisely because static, point-in-time models fail to capture evolving technology loss channels. Build update cadences into your model governance.

Build auditability in from the start. The evidence trail your digital asset audit processes produce should connect directly to model inputs and outputs. Regulators will ask to see the data behind the score, and your governance structure should make that retrieval straightforward.

Pro Tip: When integrating risk automation into existing governance, treat the automated decision layer as a model in its own right. It needs validation documentation, change management processes, and periodic review just like any other model in your model risk management inventory.

My take on building risk models that actually hold up

I’ve spent years watching organizations approach digital asset risk from two equally flawed positions. The first is pretending existing models need only minor tweaks. The second is insisting everything must be rebuilt from scratch. Both miss the point.

What I’ve found in practice is that the fundamental principles of risk management, materiality, evidence, governance, and defensibility, transfer completely to digital assets. What doesn’t transfer is the assumption that your data inputs are already defined and your operational failure modes are the familiar ones. Those assumptions were never written down because they didn’t need to be in traditional finance. In digital asset contexts, you have to make them explicit before you can override them.

The hardest lesson I’ve learned is about automation balance. Teams that automate too aggressively find themselves unable to explain decisions in examination. Teams that refuse to automate find themselves drowning in volume. The right position is deliberate: automate the high-volume, policy-clear decisions with traceable evidence, and preserve human review for the ambiguous, high-value cases where judgment adds real value.

My contrarian view on the current debate: the call to scrap existing risk frameworks is mostly driven by vendors selling new tools, not by practitioners managing real exposure. Don’t buy it. Adapt your models with rigor, document your reasoning, and build the governance infrastructure to make those models defensible. That’s what regulators will reward, and it’s what your institution actually needs.

— Gregg

Sharpen your digital asset risk readiness with DARE

Adapting risk models for digital assets requires more than reading about it. It requires structured assessment, documented competency, and a governance framework that holds up under regulatory scrutiny.

Wush offers the Digital Asset Readiness Evaluation (DARE), a certification built specifically for finance professionals, risk managers, and treasury teams managing digital asset exposure. DARE covers risk management, operational controls, custody, regulatory compliance, and the governance structures discussed throughout this article. The certification includes modular learning, formal assessment, and annual renewal to keep your credentials current as the regulatory and technological environment shifts. For professionals looking to demonstrate a competitive edge in digital asset risk readiness, DARE provides the structured framework your institution needs.

FAQ

What makes digital asset risk models different from traditional ones?

Digital asset risk models require different data inputs, including on-chain flow data, wallet-level scoring, and smart contract audit status, rather than a wholesale new framework. The core principles of evidence-based risk management still apply.

Why do risk decisions in crypto require automation?

The volume of on-chain decisions exceeds human processing capacity, and regulators require traceable evidence behind each decision, making defensible automation a practical necessity rather than a convenience.

What is the Basel III risk weight for Bitcoin?

Basel III assigns a 1250% risk weight to BTC and similar crypto assets, making granular, documented risk models a capital efficiency issue for institutional holders.

How does blockchain transparency affect risk scoring?

Blockchain’s public ledger enables multi-hop tracing across dozens of wallets and chains, creating richer evidence patterns than fiat systems but also exposing new obfuscation techniques like chain peeling and cross-chain laundering that models must account for.

What is the first step in adapting an existing risk model for digital assets?

Shift your unit of analysis from legal entity or account to wallet and flow-graph level. Models that score only at the counterparty level will systematically miss illicit exposure origins in blockchain transaction paths.