Digital Asset Third Party Security Audit: 2026 Guide

A digital asset third-party security audit is a structured evaluation of a vendor’s controls, governance, and compliance practices to verify that the security of your organization’s digital asset operations meets regulatory and institutional standards. Finance, legal, and compliance professionals increasingly treat this process as a non-negotiable component of third-party risk management, not a one-time checkbox. The stakes are concrete: weak vendor controls create inherited risk that regulators now scrutinize directly. This guide covers every phase of the process, from prerequisites and execution to ongoing monitoring, using current methodologies including NIST CSF v2, KY3P, and SOC 2 Type II.

What does a digital asset third party security audit actually require?

The formal industry term for this practice is third-party risk assessment (TPRA), though “security audit” is the language most commonly used in vendor contracts and regulatory correspondence. Both terms describe the same core process: independently verifying that a vendor’s controls operate as claimed, not just as documented.

Due diligence for third-party security in digital assets extends well beyond onboarding. Interagency 2023 guidance requires continuous diligence across all vendor lifecycle phases, with documented evidence of monitoring and subcontractor management. This means your audit program must cover initial onboarding, periodic reassessment, and event-triggered reviews triggered by incidents, ownership changes, or regulatory updates.

The scope of a digital asset security review is broader than most compliance teams expect. Audit engagement scope for digital assets extends beyond code to operational controls, regulatory compliance, governance design, and privacy protections. A vendor providing custody infrastructure, for example, requires evaluation of its key management procedures, incident response plans, and access control architecture, not just its smart contract code.

Three frameworks anchor most credible audit programs in 2026. NIST CSF v2 organizes governance, risk assessment, and control evaluation across five core functions: Govern, Identify, Protect, Detect, and Respond. ISO 27001:2022 provides the information security management system baseline. PCI DSS 4.0 applies wherever payment card data intersects with digital asset workflows. NIST CSF’s five core functions map directly to digital asset risks, making it the most practical starting framework for structuring audit scope.

How to prepare before launching a third-party security assessment

Preparation determines whether your audit produces defensible evidence or a document that satisfies no one. The following prerequisites are non-negotiable before fieldwork begins.

Documentation to collect from the vendor before day one:

- Current SOC 2 Type II report (covering at least a 6-month testing window)

- Most recent penetration test results with remediation evidence

- Incident response policy and the last tabletop exercise record

- Subcontractor and fourth-party disclosure list

- Business continuity and disaster recovery plans

Frameworks to map your audit scope against:

- NIST CSF v2 for governance and risk structure

- ISO 27001:2022 for information security management

- PCI DSS 4.0 where payment workflows intersect

The AWS KY3P assessment is a standardized, evidence-based methodology covering 200+ controls that maps to NIST CSF v2, PCI DSS 4.0, and ISO 27001:2022. For cloud and infrastructure vendors handling digital assets, requesting a KY3P evidence package reduces the due diligence burden significantly while providing validated control evidence your risk committee will accept.

Contractual audit rights are the legal foundation of the entire process. Before engaging any digital asset vendor, confirm that your master service agreement grants explicit rights to conduct security audits, receive subcontractor disclosures, and require remediation within defined timeframes. Vendors who resist these clauses during contract negotiation are signaling a risk posture worth noting before any assets change hands.

Pro Tip: Request the vendor’s most recent third-party audit report during contract negotiation, not after signing. Vendors who cannot produce a SOC 2 Type II report or equivalent within 30 days of request should be classified as elevated risk regardless of their sales representations.

| Preparation item | Why it matters |

|---|---|

| SOC 2 Type II report | Proves controls operated continuously, not just at a point in time |

| KY3P evidence package | Reduces redundant questionnaires for cloud infrastructure vendors |

| Subcontractor disclosure | Surfaces fourth-party risk before it becomes your liability |

| Contractual audit rights | Gives legal standing to demand evidence and require remediation |

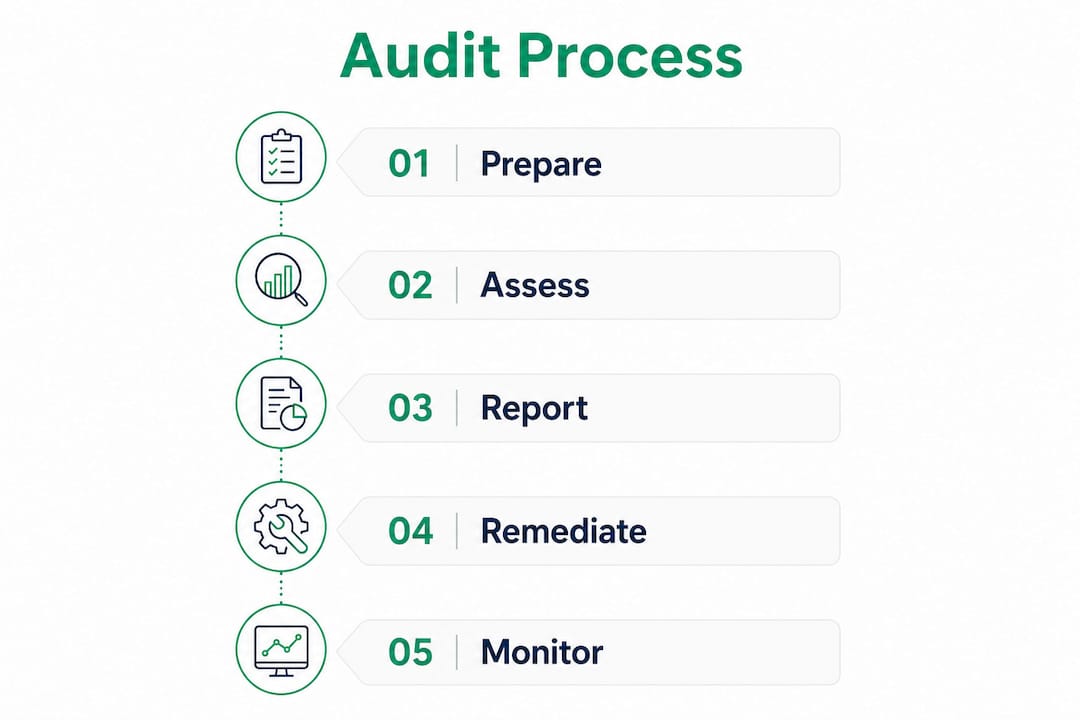

How to execute a digital asset security review step by step

Execution follows a logical sequence. Skipping steps or reordering them creates gaps that regulators and internal audit committees will identify.

-

Define scope and risk tier. Classify the vendor by the sensitivity of assets and data they access. Custody providers and blockchain node operators warrant the most intensive review. API aggregators and analytics tools require proportionally less scrutiny.

-

Review technical controls. For blockchain-native vendors, this includes smart contract code review, key management architecture, and wallet infrastructure security. For infrastructure vendors, focus on network segmentation, encryption standards, and patch management cadence.

-

Assess operational security. Evaluate incident response procedures, access control policies, and privileged user management. Cryptocurrency partners’ weak controls create inherited third-party risk, and FTI’s 2026 guidance specifically recommends aligning control measurements with your organization’s broader risk policies to withstand regulatory scrutiny.

-

Evaluate compliance management programs. Confirm the vendor maintains an active compliance function, not just a policy library. Request evidence of staff training completion, audit log retention, and regulatory change management procedures.

-

Review governance design. Assess whether the vendor’s board or executive leadership receives regular security reporting. Vendors with no governance structure above the CISO level represent a structural risk regardless of their technical controls.

-

Validate evidence quality. Continuous security programs that integrate multiple assessment layers with SOC 2 Type II and privacy protections are becoming the standard expectation from financial supervisors. OpenZeppelin’s program is one example of how vendors can produce ongoing auditable evidence rather than static point-in-time reports.

-

Document findings and assign risk ratings. Use a consistent rating scale (Critical, High, Medium, Low) and map each finding to the relevant framework control. This output feeds directly into your risk committee reporting and regulatory documentation.

Pro Tip: When reviewing incident response procedures, ask the vendor to walk you through their last actual incident, not a tabletop scenario. The gap between documented procedure and operational reality is where the real risk lives.

The digital asset audit trail checklist for enterprise teams provides a practical reference for structuring evidence collection during each of these steps.

Common pitfalls in third-party risk management for digital assets

Most audit failures are predictable. The following patterns appear repeatedly across finance and compliance teams conducting their first or second digital asset security review.

Scope creep in both directions. Over-scoping wastes resources and delays findings. Under-scoping misses the controls that actually matter. Define scope in writing before fieldwork begins and require sign-off from legal, compliance, and the business owner.

Point-in-time evidence accepted as sufficient. Point-in-time audit reports frequently create friction with reviewers who expect ongoing evidence of controls operation. Mature audits produce Type II style evidence over a testing window. A vendor who offers only a penetration test from eight months ago is not providing the evidence standard that risk committees now expect.

Fourth-party risk ignored. Most fintech partners rely on their own third parties, creating additional risk layers that require evaluation during digital asset third-party audits. If your custody vendor uses a cloud provider that has never been assessed, that gap is your exposure. Require vendors to disclose all material subcontractors and provide evidence of their own third-party oversight programs.

Vendor attestations accepted without validation. A vendor completing a security questionnaire is not the same as a vendor demonstrating control operation. Combining questionnaires, on-site visits, and ongoing monitoring best reflects the vendor’s current security posture. Bitsight and similar security rating platforms provide objective, data-driven vendor risk metrics that supplement self-reported attestations.

Regulatory defensibility requires evidence that controls operated continuously, not just that policies existed. When a vendor cannot produce operational evidence, treat the gap as a finding, not an administrative delay.

Pro Tip: Build a vendor refusal protocol into your audit program before you need it. Define in advance what happens when a vendor declines an on-site visit or refuses to disclose subcontractors. Having a documented escalation path prevents the situation from stalling indefinitely.

How to integrate audit results into ongoing enterprise risk management

A completed audit report has limited value unless it connects to a live risk management workflow. The integration phase is where most organizations lose momentum.

Auditability and compliance readiness is tied to operational resilience, governance frameworks, documentation, training, monitoring, and regular audits as core validation components. Fireblocks’ compliance glossary identifies these as the recurring artifacts that demonstrate compliance during regulatory examinations. Your audit outputs should map directly to these categories.

Ongoing monitoring tools to deploy after audit completion:

- Automated security rating platforms (Bitsight, SecurityScorecard) for continuous vendor risk signals

- Contract-triggered review clauses activated by incidents, ownership changes, or material control failures

- Quarterly vendor performance scorecards aligned to the audit’s risk ratings

- Annual reassessment cycles with interim reviews for critical vendors

Aligning audit outputs with board reporting is the step most compliance teams defer too long. The board-level digital asset oversight checklist for 2026 provides a practical structure for translating audit findings into the governance reporting format that directors and supervisors expect.

Crypto ecosystems increase access points through third and fourth parties, requiring broader audit scopes and deeper due diligence over time. As your vendor ecosystem grows, the monitoring program must scale proportionally. A static annual audit cycle is insufficient for vendors with direct access to custody infrastructure or transaction signing keys.

Technology platforms that maintain an audit trail of vendor assessments, evidence packages, and remediation tracking reduce the administrative burden of demonstrating compliance to regulators. Building this infrastructure early, before a regulatory examination, is significantly less costly than reconstructing it under pressure.

Key takeaways

A digital asset third-party security audit requires continuous, evidence-based oversight across the full vendor lifecycle, not a single point-in-time review.

| Point | Details |

|---|---|

| Scope beyond code review | Audits must cover operational controls, governance, compliance programs, and privacy protections. |

| Demand continuous evidence | SOC 2 Type II and KY3P packages prove controls operated over time, satisfying risk committees. |

| Address fourth-party risk | Require vendors to disclose subcontractors and evidence their own third-party oversight programs. |

| Integrate findings into governance | Map audit outputs to board reporting and compliance documentation to maintain regulatory defensibility. |

| Monitor continuously | Deploy security rating tools and contract triggers to maintain visibility between formal audit cycles. |

Why the audit bar is higher than most teams realize

I’ve reviewed dozens of vendor assessment programs across financial institutions entering the digital asset space, and the pattern is consistent: teams underestimate how much regulators have moved the goalposts in the last 18 months. The expectation is no longer a completed questionnaire and a SOC 2 report. Supervisors want to see evidence that controls operated continuously, that subcontractor risk was actively managed, and that findings from prior audits were actually remediated.

The shift toward continuous security programs is not a vendor marketing trend. It reflects a genuine regulatory expectation that finance and compliance teams are only beginning to internalize. OpenZeppelin’s model, where ongoing assessment layers produce auditable evidence rather than static snapshots, is the direction the entire field is moving. Teams that build their vendor oversight programs around point-in-time audits will face increasing friction with internal audit, risk committees, and external examiners.

The fourth-party problem is the one that surprises most compliance officers. Your custody vendor’s cloud provider, their identity management vendor, their backup infrastructure provider: all of these represent exposure that flows back to your organization. Mapping that chain and requiring your vendors to manage it is not optional in 2026. It is the work.

My practical advice: treat your first digital asset third-party security audit as a baseline-setting exercise, not a pass/fail event. Use it to understand where your vendor ecosystem actually stands, build the monitoring infrastructure, and establish the evidence collection cadence that will satisfy regulators when they ask. The organizations that do this proactively are the ones that avoid the remediation scramble later.

— Gregg

How DARE supports your audit readiness and compliance program

Wush’s Digital Asset Readiness Evaluation (DARE) is built specifically for the governance and compliance gap that third-party security audits expose. Finance, legal, and risk professionals use the DARE certification program to build the structured frameworks, documented evidence, and institutional credentials that regulators and risk committees expect. The program covers custody, regulatory compliance, risk management, legal controls, and operational security in a modular format with annual renewal to keep pace with evolving standards. If your organization is preparing for a vendor audit cycle or needs to demonstrate audit readiness to a supervisor, DARE provides the structured foundation that ad hoc programs cannot. Learn more about your competitive edge with a structured audit preparation framework.

FAQ

What is a digital asset third-party security audit?

A digital asset third-party security audit is a formal evaluation of a vendor’s security controls, governance practices, and compliance programs to verify they meet the standards required for safe digital asset operations. It covers technical, operational, and regulatory dimensions, not just code or infrastructure.

How is this different from a standard cybersecurity audit?

A standard cybersecurity audit focuses on an organization’s own controls. A third-party security assessment evaluates a vendor’s controls as they affect your organization’s risk exposure, including subcontractor (fourth-party) risk that flows through the vendor’s own supply chain.

What evidence standard do regulators expect?

Regulators and risk committees increasingly expect Type II style evidence proving controls operated continuously over a defined testing window, not point-in-time reports or vendor attestations alone. SOC 2 Type II reports and KY3P evidence packages are the current benchmarks.

How often should digital asset vendors be reassessed?

Critical vendors with direct access to custody infrastructure or transaction signing keys warrant annual formal reassessment with continuous monitoring between cycles. Lower-risk vendors may follow an 18 to 24 month cycle, with event-triggered reviews for incidents or material changes.

What happens if a vendor refuses to cooperate with an audit?

Vendor refusal should be treated as a risk finding and escalated through the contractual remediation process. If audit rights are embedded in the master service agreement, non-cooperation is a contract breach. Organizations should have a documented escalation and exit protocol before this situation arises.